Pensions are one of the cornerstones of social security systems worldwide. They provide a financial safety net for individuals in their retirement years, ensuring they can maintain a basic standard of living after leaving the workforce. Across the globe, pensions constitute a significant portion of government social security expenditures. In countries like Germany, Japan, and the United States, pensions make up more than half of the social security budget, often accounting for a substantial percentage of GDP. For instance, in 2021, Japan spent over 10% of its GDP on public pensions, reflecting the importance of this benefit in ensuring economic stability for retirees.

Pensions also serve a broader societal purpose. They reduce poverty among the elderly, ensure dignity in retirement, and promote intergenerational equity. Without robust pension systems, a significant portion of the aging population would fall below the poverty line, increasing reliance on other forms of public assistance. For developing countries, implementing pension systems has become an essential tool for reducing inequality and promoting sustainable development. However, the growing burden of pension payments poses serious challenges for many nations.

The Burden of Pension Payments on Social Security Systems

While pensions provide critical support, they also place immense financial pressure on governments. Many countries face a mounting pension bill driven by aging populations, longer life expectancies, and declining birth rates. In developed nations, where populations are aging rapidly, the ratio of working-age individuals to retirees is shrinking, creating significant financial strain on pension systems.

For example, in the United States, the Social Security Trust Fund is projected to face a shortfall by the mid-2030s, with reserves potentially running out if no policy adjustments are made. Similarly, in Europe, countries like Italy and France face rising pension costs that exceed their ability to fund these programs sustainably. This imbalance threatens the solvency of many national pension systems, raising concerns about the future of social security benefits.

Population Shifts and the Insolvency Risk

The demographic transition occurring in many parts of the world highlights the structural challenges of sustaining pension systems:

- Aging Populations: As life expectancy increases, individuals spend more years in retirement, increasing the financial burden on pension systems. For example, the average life expectancy in Japan is over 84 years, leading to prolonged pension payouts.

- Declining Birth Rates: In countries like Germany and South Korea, declining birth rates mean fewer workers are contributing to the system, reducing the funds available for payouts.

- Shrinking Workforce: As fewer people enter the workforce, the ratio of contributors to beneficiaries continues to decline, undermining the pay-as-you-go structure of many pension systems.

Without reform, these trends could lead to the insolvency of social security systems, jeopardizing the retirement security of millions.

Private vs. National Pension Systems

The challenges faced by public pension systems have led to the growth of private pension schemes as a supplementary or alternative option in many countries. While national pensions are typically mandatory and funded through payroll taxes, private pensions are often voluntary and funded by individual contributions or employer-sponsored plans.

National Pensions

National pension systems are typically managed by governments and funded through contributions from both employees and employers. These systems aim to provide universal coverage and basic income security for retirees. Examples include:

- Social Security in the United States: A federal program funded through payroll taxes, providing retirement, disability, and survivor benefits.

- State Pension in the UK: A government-run scheme based on National Insurance contributions, offering a fixed payout upon reaching retirement age.

- Japan’s Public Pension System: A two-tier system combining a basic pension and an earnings-related pension.

Private Pensions

Private pensions, such as 401(k) plans in the United States or occupational pensions in the UK, allow individuals to save for retirement independently of national systems. These plans often include employer contributions and are subject to market performance, which can influence retirement payouts. Private pensions provide flexibility and additional income security but also come with investment risks and administrative costs.

The reliance on private versus national pensions varies significantly by region. In the US, private pensions are a critical component of retirement planning, while in much of Europe, public pensions dominate. Developing nations often rely more heavily on informal family support systems, though private pensions are gaining traction as economies formalize.

Regional Differences in Pension Systems

Pension systems differ widely across regions, reflecting variations in economic structures, demographic trends, and cultural norms. For example:

- Europe: Most countries rely on generous public pension systems funded through high taxes. Countries like Germany and France have robust social security systems but face sustainability challenges due to aging populations.

- Asia: Countries like Japan and South Korea have public pension systems but are increasingly encouraging private savings due to demographic pressures.

- Africa: Pension coverage remains low, with many workers in the informal sector. Efforts are underway to expand coverage through contributory schemes and social pensions.

- Caribbean: Most social security systems in the Caribbean provide both pensions and age grants, with age grants being awarded to those beneficiaries who did not contribute enough to qualify for a regular age pension but did meet the minimum contribution threshold to be entitled to one-time lump-sum age benefit.

These regional differences underscore the need for flexible and adaptable pension administration systems, such as Interact SSAS, which can accommodate varying rules and structures.

The Complexity of Pension Calculations

Calculating pensions is a complex process that requires extensive historical data, including employment records, contribution histories, and average earnings. The complexity is further heightened by variations in rules across different types of pensions. Common types include:

- Age Pensions: Regular payouts (monthly or semi-monthly) based on reaching retirement age and meeting contribution thresholds.

- Age Grants: Lump-sum payments for individuals who do not qualify for full pensions but have made some contributions.

- Survivor Pensions: Benefits paid to dependents of deceased contributors.

- Disability Pensions: Benefits for individuals unable to work due to disability.

The calculation methods differ significantly. Age pensions often rely on factors like average annual or weekly earnings and total contributions, while survivor pensions consider the contributor’s history and the beneficiaries’ relationships. Age grants use simpler formulas, often based on the number of contribution blocks.

Example: Pension Calculations in Dominica

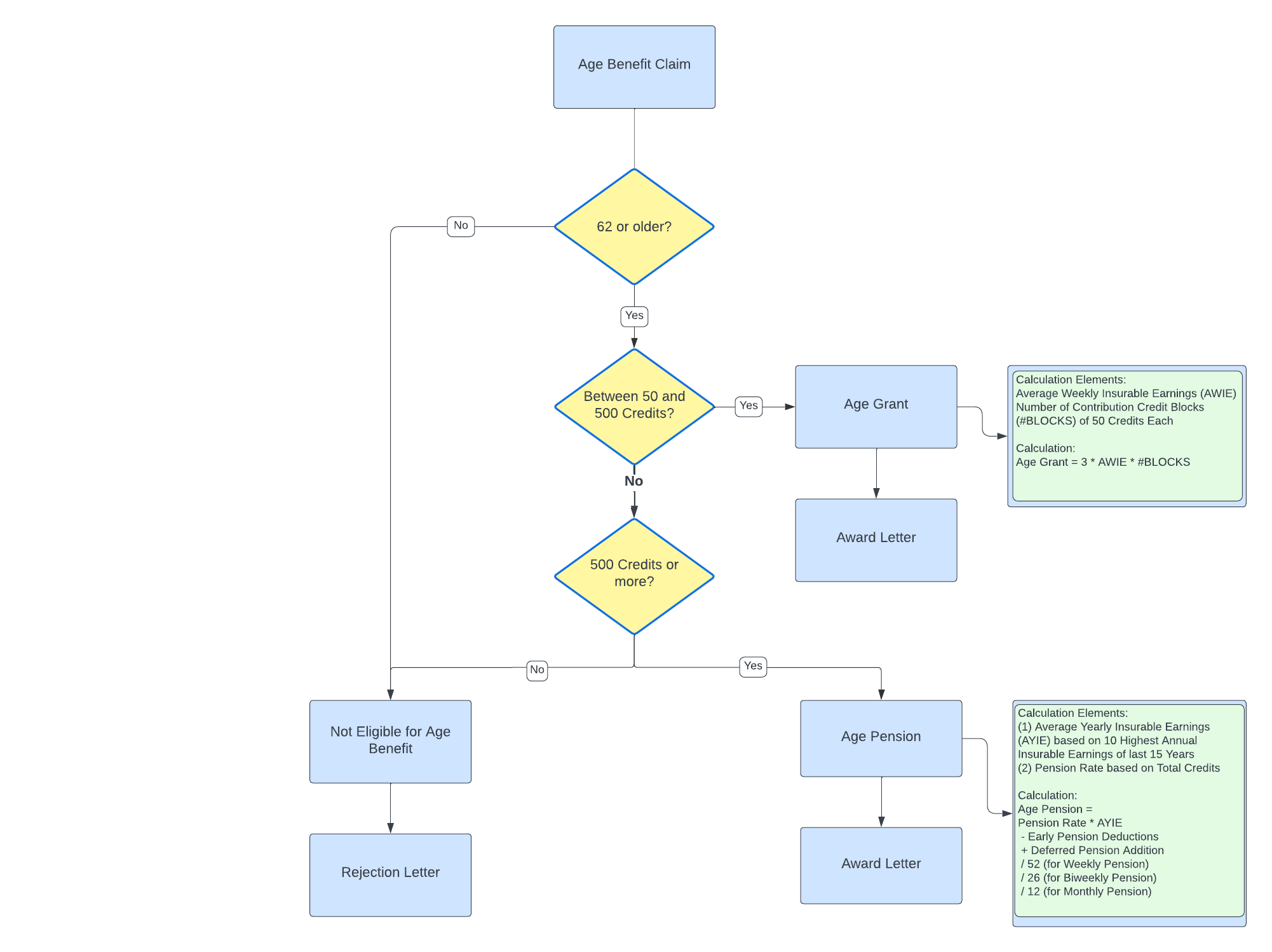

Dominica provides a clear example of how age pensions and age grants are calculated:

- Age Pension: To qualify, an individual must have at least 500 contribution credits. The pension amount is based on the Average Yearly Insurable Earnings (AYIE) from the highest ten years out of the previous 15 years of a contributor’s career and a pension rate determined by total credits. For example:

- AYIE = $20,000

- Pension Rate = 40%

- Annual Pension = $20,000 x 0.4 = $8,000

- Monthly Pension = $8,000 ÷ 12 = $666.67

- Age Grant: For individuals with 50-499 credits, the grant is calculated as:

- Age Grant = 3 x Average Weekly Insurable Earnings (AWIE) x Number of 50-Credit Blocks

- Example: AWIE = $350, Total Credits = 400 (8 blocks)

- Age Grant = 3 x $350 x 8 = $8,400

Figure 1: Pension Calculation Example in Interact SSAS Setup

How Interact SSAS Supports Pension Administration

Interact SSAS simplifies pension management with robust, configurable features that cater to diverse rules and requirements:

- Policy Configuration: Administrators can define benefit classes, policies, and entitlement rules to reflect local laws and organizational needs. This flexibility supports various pension types, including age pensions and survivor benefits.

- Data Integration: Historical contribution data is seamlessly integrated, enabling accurate calculations for even the most complex scenarios.

- Automated Workflows: From application submission to benefit disbursement, the system automates processes to reduce errors and administrative burden.

- Regional Adaptability: Interact SSAS accommodates regional variations, such as CARICOM’s totalization agreements, ensuring compliance with international treaties.

How Interact SSAS Supports Pension Administration

Interact SSAS is a comprehensive system designed to simplify and enhance the administration of pension benefits. It caters to the diverse rules and requirements of pension schemes worldwide by providing robust, configurable features that streamline processes and ensure accuracy. Here’s how Interact SSAS addresses some of the most complex aspects of pension management:

Policy Configuration for Any Pension Type

Administrators can define unlimited benefit classes, policies, and entitlement rules to reflect local laws and organizational requirements. This flexibility allows the system to accommodate various types of pensions, including:

- Age Pensions: Regular payouts for retirees who meet specific age and contribution thresholds.

- Survivor Benefits: Payments to dependents of deceased contributors.

- Age Grants: Lump-sum payments for individuals with insufficient contributions for a full pension.

Support for Minimum Pension

To ensure a basic level of financial security, many pension systems include a minimum pension provision, guaranteeing that eligible retirees receive no less than a predefined amount, regardless of their contribution history. Interact SSAS allows administrators to configure minimum pension thresholds as part of the benefit entitlement rules. For example:

- Minimum pension thresholds can be set based on local laws or organizational policies.

- The system automatically applies the minimum pension rule during benefit calculations, ensuring compliance with the established limits.

This feature is critical in addressing poverty among retirees, especially in regions where contribution records may be incomplete or sporadic due to informal employment sectors.

Pension Rate Adjustments

Pension rates often vary based on factors like contribution totals, years of service, or government-mandated adjustments. Interact SSAS enables dynamic pension rate adjustments, allowing the system to apply planned periodic adjustments mandated by legislation or inflation indices.

Early Pension Reduction Factor

Many pension systems allow individuals to claim pensions before reaching the standard retirement age, with a corresponding reduction in benefits to account for the longer payout period. Interact SSAS supports the configuration of an early pension reduction factor, which:

- Reduces the pension amount based on the number of months or years the claimant is below the standard retirement age.

- Ensures that the system automatically calculates the reduced pension amount during processing. For instance, if the standard reduction is .5% per month below retirement age, the system calculates the reduced rate seamlessly, ensuring consistency and accuracy.

Deferred Pension Increased Annual Factor

Conversely, some pension schemes reward individuals who defer their pension beyond the standard retirement age by increasing the annual benefit amount. Interact SSAS includes support for a deferred pension increased annual factor, which:

- Calculates and applies an increment for each year the pension is deferred.

- Encourages individuals to delay claiming their pension, potentially reducing strain on the pension fund. For example, if a deferred pension increases by 6% per year, the system applies this factor to the final calculation, ensuring the individual receives the appropriate higher benefit.

No Two Full Pension Rule

To prevent double-dipping and ensure equitable distribution of resources, many pension systems enforce a No Two Full Pension rule. This rule stipulates that if an individual qualifies for more than one pension (e.g., an age pension and a survivor pension), they are entitled to the higher of the two and a partial amount of the other. Interact SSAS fully supports this rule by:

- Automatically identifying cases where individuals qualify for multiple pensions.

- Ensuring compliance with the rule by calculating the higher pension in full and a fraction (e.g., 50%) of the other. For instance, if an individual qualifies for an age pension of $1,000 and a survivor pension of $800, the system automatically calculates $1,000 + $400 (50% of the survivor pension), ensuring transparency and accuracy.

Accurate Calculations with Historical Data

Pension calculations often require decades of historical data, including contribution records and average earnings. Interact SSAS seamlessly integrates historical data to ensure precise benefit calculations. The system:

- Pulls data from integrated databases, minimizing manual errors.

- Accommodates complex scenarios, such as totalizing contributions from multiple jurisdictions under agreements like the CARICOM Agreement.

Automation of Complex Processes

Interact SSAS automates the entire pension management process, from application submission to benefit disbursement. Key automation features include:

- Workflow Automation: Streamlines approvals and ensures timely processing of applications.

- Dynamic Calculations: Handles multi-step calculations for age pensions, age grants, and survivor benefits.

- Policy Compliance: Ensures all calculations and disbursements align with predefined rules and regulations.

Document Management and Verification in the Digital Age

An integral part of pension administration is managing and verifying the documents required for benefit eligibility. Historically, this has been a time-consuming and paper-intensive process, but modern systems like Interact SSAS have transformed this into a seamless digital workflow. The Document Management System (DMS) integrated into Interact SSAS enables social security organizations to handle all documentation electronically, reducing administrative overhead and improving the user experience.

For example, beneficiaries applying for age pensions can now submit their Certificates of Life digitally, eliminating the need for physical submissions. These documents can be generated through the system and authenticated with digital signatures, ensuring security and validity. Similarly, medical documentation for disability benefits—such as assessments, certifications, or periodic updates—can be uploaded directly via the self-service portal, where claimants or authorized medical professionals can fill out electronic forms and attach supporting files.

For survivor benefits, dependent children can submit school certificates or proof of enrollment electronically, ensuring continued eligibility without requiring paper documents. The system supports:

- Electronic Form Submissions: Information can be captured through online forms integrated into the portal, allowing beneficiaries and third parties (e.g., doctors or schools) to provide required data easily.

- Digital Signatures: Secure authentication methods validate the authenticity of documents without the need for physical signatures.

- Automated Workflows: Submitted forms are routed automatically to the appropriate personnel for review and approval, significantly speeding up the process.

- Document Verification and Alerts: The system sends automated reminders to beneficiaries about upcoming deadlines for submitting verification documents, such as Certificates of Life or updated school enrollment certificates.

By enabling electronic submission and processing of documentation, Interact SSAS not only reduces reliance on paper but also enhances accessibility for beneficiaries. This innovation ensures compliance with regulatory requirements while significantly improving efficiency, accuracy, and transparency in the management of pension and other benefit-related documents.

Streamlined Application and Review

Interact SSAS simplifies the application process for pensions by:

- Digitizing applications and integrating them with the system’s workflows.

- Validating supporting documents against eligibility criteria.

- Automating the approval process, reducing administrative delays.

Regional Adaptability

One of Interact SSAS’s standout features is its ability to adapt to regional variations in pension rules. For example:

- CARICOM Agreement Support: The system can totalize contributions across member states, ensuring individuals who have worked in multiple countries receive fair benefits.

- Customizable Policies: Administrators can configure policies to reflect local laws, such as Dominica’s unique rules for age grants and pensions.

Linking Pensions to Broader Social Security Goals

Pensions play a critical role in achieving broader social security objectives, such as reducing poverty, promoting economic stability, and ensuring equity. Effective pension administration is essential for maintaining public trust and ensuring that benefits are delivered accurately and on time. Systems like Interact SSAS not only enhance operational efficiency but also support strategic planning, helping social security organizations adapt to demographic and economic challenges.

Conclusion

Pensions are a vital component of social security systems, providing financial stability for retirees and fostering societal equity. However, the growing burden of pension payments, combined with demographic shifts, poses significant challenges for governments worldwide. The complexity of pension calculations and the diversity of systems across regions necessitate advanced solutions like Interact SSAS, which offers the flexibility and functionality required to manage these critical benefits effectively. By automating processes, ensuring compliance, and adapting to local rules, Interact SSAS supports social security organizations in delivering pensions efficiently and equitably, ensuring a secure future for beneficiaries and the sustainability of the system.