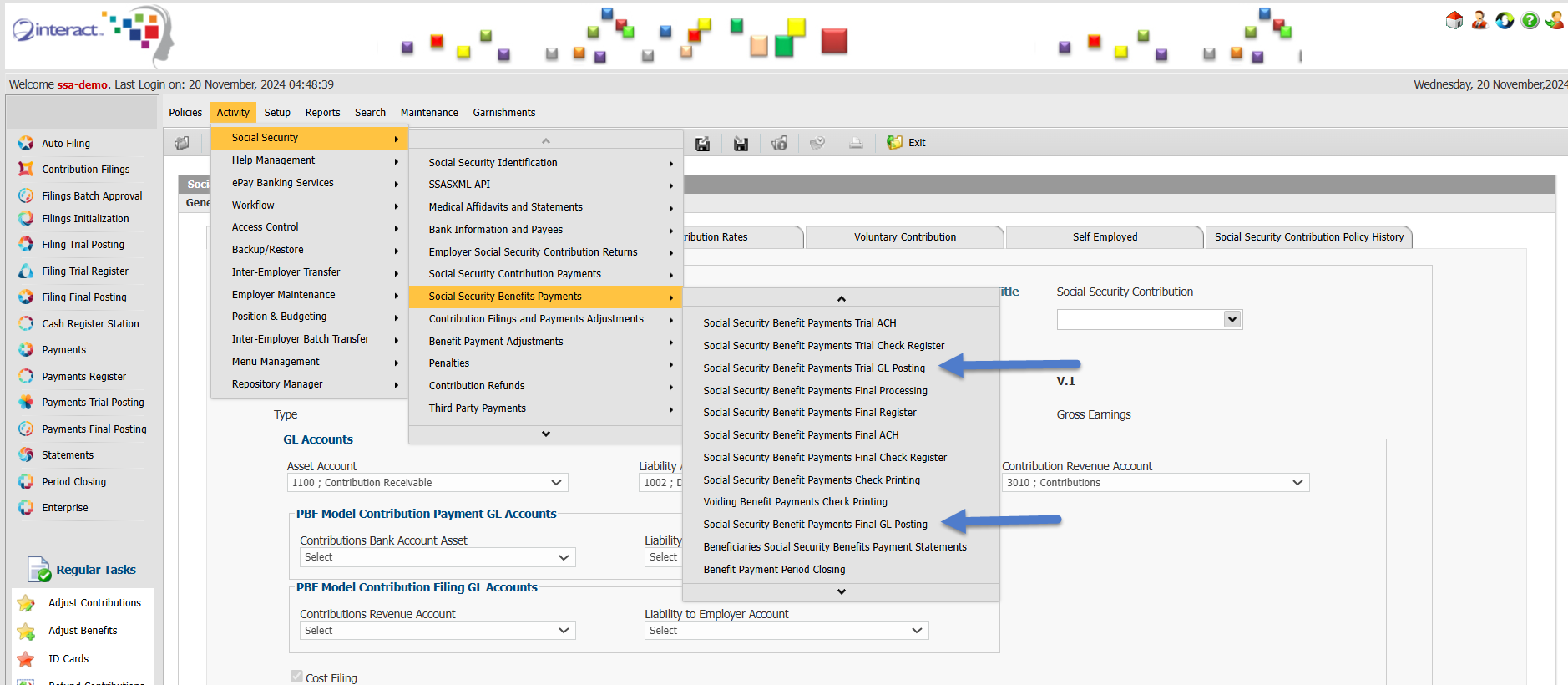

Figure 1: Trial GL Posting and Final GL Posting Menus for Benefit Payments

The management of financial transactions in social security systems is critical for maintaining transparency, accountability, and operational efficiency. A seamless General Ledger (GL) interface is essential for social security administration systems, as it enables accurate financial reporting, compliance with regulatory requirements, and integration with various accounting systems. This blog explores why a robust GL interface is a necessity, examines challenges faced by social security systems in countries like the United States, Canada, and the Caribbean, and provides an in-depth look at the GL interface capabilities of Interact SSAS.

Challenges in Financial Management for Social Security Administrations

- Diverse GL Systems Across Government Organizations

Government agencies, including social security administrations, often use a variety of GL systems:

- Legacy Systems: Many organizations rely on older, custom-built accounting systems that may not support modern file formats or integrations.

- Modern Accounting Solutions: Others utilize commercial software like SAP, Oracle Financials, or even QuickBooks, each with its specific data formats.

- Custom-Built Systems: In some cases, agencies use bespoke solutions tailored to their unique needs.

The lack of standardization across these systems creates challenges in ensuring financial data is accurately recorded and seamlessly integrated with the accounting frameworks of external stakeholders.

- Complex Reporting Requirements

Social security administrations must report to various entities, including:

- National Governments: For compliance with fiscal and regulatory standards.

- International Organizations: Such as the World Bank or IMF for financial monitoring.

- Actuarial Committees: For evaluating fund sustainability and projecting long-term viability.

- Public Auditors: To demonstrate fiscal accountability and prevent misuse of funds.

Each entity often requires different formats, levels of detail, and periodic submissions, adding complexity to the financial reporting process.

- Importance of Accurate Accounting

Accurate accounting records are essential for:

- Budgeting and Forecasting: Ensuring that social security funds remain solvent and can meet future obligations.

- Auditing and Transparency: Enabling internal and external audits to maintain public trust.

- Investment Fund Management: Ensuring investment portfolios are balanced to sustain long-term benefits.

Inaccuracies in accounting can lead to regulatory fines, loss of trust, and challenges in managing social security investment funds.

The Role of a Seamless GL Interface

A seamless GL interface addresses these challenges by automating and standardizing the generation and posting of journal entries to the GL. Key benefits include:

- Automated GL Transactions

Automating GL entries ensures that every transaction—whether a contribution received or a benefit paid—is recorded accurately. This eliminates manual errors, reduces administrative burden, and speeds up reconciliation processes.

- Compatibility with Legacy and Modern Systems

A robust GL interface supports multiple file formats, enabling seamless integration with both legacy systems and modern accounting platforms. This ensures continuity even in organizations using outdated infrastructure.

- Real-Time Financial Reporting

With GL transactions posted in real-time or near real-time, financial reports are always up-to-date, enabling timely decision-making.

- Scalability

Social security systems often handle vast volumes of transactions. A scalable GL interface can process large datasets efficiently, ensuring the system grows with organizational needs.

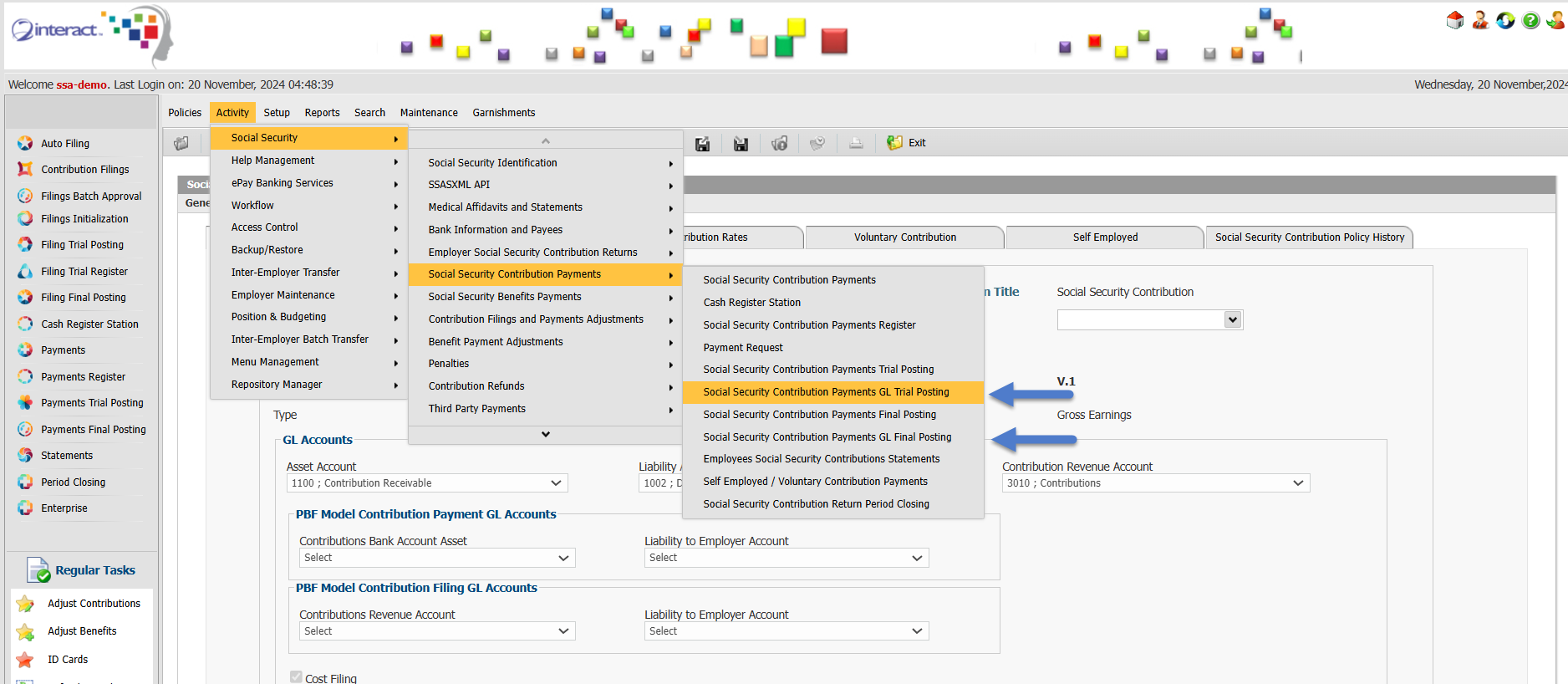

Figure 2: GL Trial and Final Posting for Contribution Payments

The General Ledger Interface of Interact SSAS

The Interact Social Security Administration System (SSAS) offers a comprehensive GL interface designed to meet the financial management needs of modern social security organizations.

Key Features of the Interact SSAS GL Interface

- Flexible GL File Formats:

- Supports standard file formats for commercial systems like SAP, Oracle and many other GLs.

- Can integrate with legacy systems using customized templates.

- GL Setup and Configuration:

- Administrators configure the GL interface to match the organization’s Chart of Accounts including the Chart of Accounts structure (including the segments and their significance) and the individual GL Accounts in use.

- Parameters include linking GL accounts to Contribution Policies, Benefit Entitlement Policies, and Penalties.

- Trial GL Files:

- Before posting transactions, SSAS generates trial GL files for review and approval.

- Administrators can identify and correct errors before finalizing entries.

- Final GL Posting:

- Once approved, trial entries are finalized and posted to the GL.

- Changes can only be made via standard adjustment processes.

The Importance of Detailed GL Account Definitions and Budgets in Social Security Administration Systems

For a social security administration, managing financial transactions efficiently and accurately is critical. Defining detailed General Ledger (GL) accounts, as illustrated in the attached screenshot, ensures clear categorization of transactions, compliance with accounting standards, and effective budgetary control. This blog explores the significance of these configurations and highlights how budgets at the account level contribute to improved financial oversight.

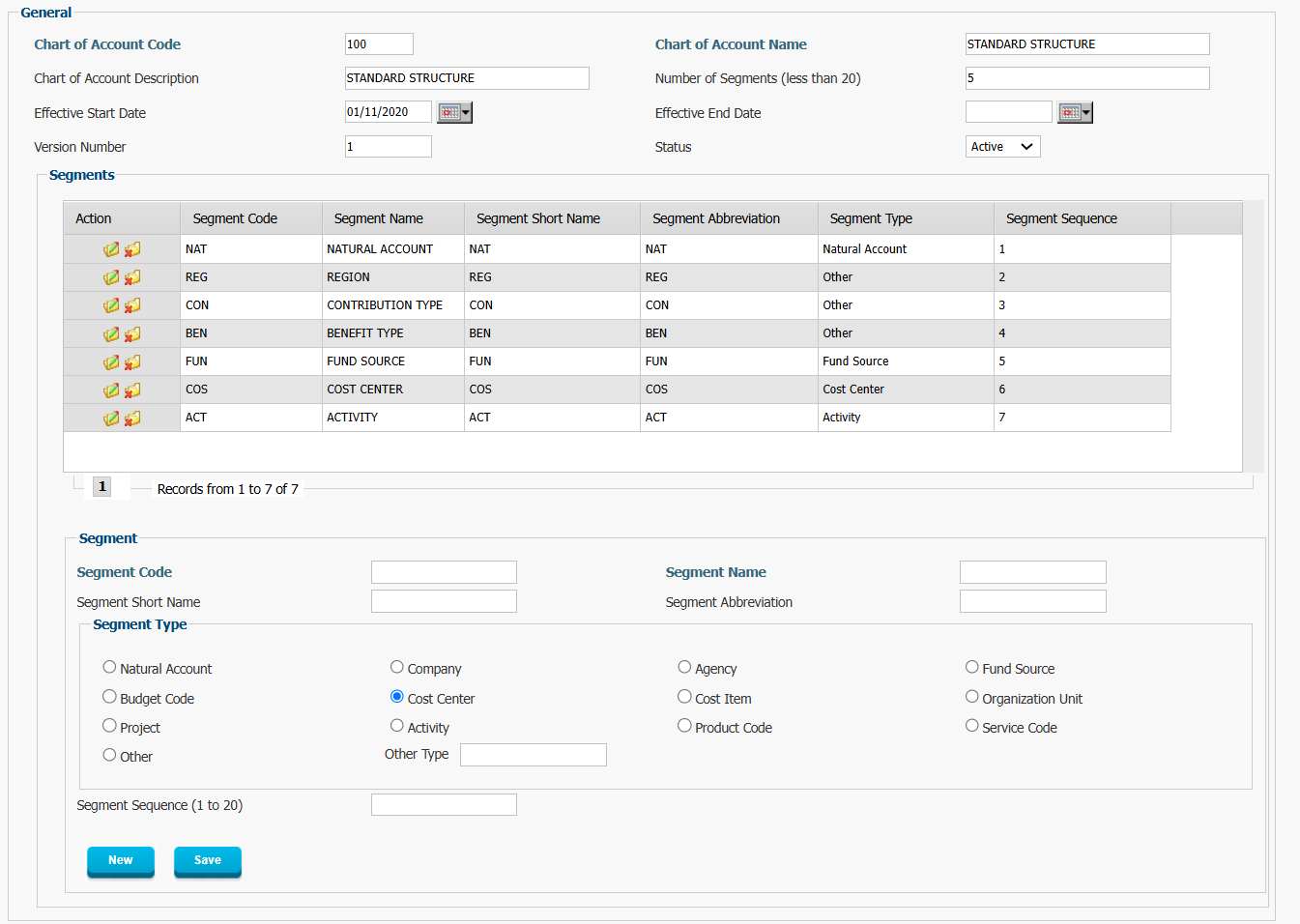

Figure 3: Chart of Account Structure configuration in financial setup of Interact SSAS

Chart of Account Structure in Interact SSAS

A Chart of Account (COA) structure, as defined in Interact SSAS (Social Security Administration System), is a foundational element of financial management and reporting. The screenshot demonstrates how administrators can configure a COA tailored to the organization’s needs by defining multiple segments. This structure enables social security administrations to capture, organize, and report financial data efficiently. Here’s an in-depth explanation of its purpose and significance:

Purpose of the Chart of Account Structure

- Standardized Financial Reporting

- A COA is a systematic and organized classification of financial accounts used for recording and reporting transactions.

- By defining specific segments, such as Natural Account, Region, Contribution Type, and Benefit Type, financial data can be recorded consistently and categorized meaningfully.

- Granular Tracking

- The segmentation allows for detailed tracking of financial transactions. For instance:

- Contributions can be tracked by Region or Contribution Type (Employee, Self-Employed, Voluntary).

- Benefit payments can be monitored by Benefit Type (Pensions, Sickness Benefits) and Fund Source.

- This ensures financial transparency and enhances decision-making capabilities.

- The segmentation allows for detailed tracking of financial transactions. For instance:

- Customizable Design for Organizational Needs

- Each social security administration has unique requirements based on its size, structure, and reporting obligations.

- The ability to define up to 20 segments, as seen in the example, ensures the COA can accommodate complex hierarchies and financial processes.

- Support for Multi-Dimensional Reporting

- Segments like Region, Cost Center, and Activity enable multi-dimensional analysis of financial data.

- This allows administrators to generate detailed reports for specific operational units, geographies, or programs.

Significance of the Defined Segments in the Chart of Account

The segments shown in the screenshot highlight how the COA structure supports comprehensive financial management.

- Natural Account

- Purpose: Defines the core type of account (e.g., assets, liabilities, income, expenses).

- Example: Cash, Contributions Receivable, Pension Expenses.

- Significance: Forms the basis for all transactions, ensuring alignment with accounting standards.

- Region

- Purpose: Tracks transactions by geographic location or operational zone.

- Example: Region 1, Region 2, Region 3.

- Significance: Enables location-specific reporting, useful for regional planning and compliance with local regulations.

- Contribution Type

- Purpose: Segments income by the type of contributor.

- Example: Employee, Self-Employed, Voluntary.

- Significance: Allows for detailed analysis of contribution revenue streams.

- Benefit Type

- Purpose: Categorizes expenses by the type of benefit.

- Example: Pensions, Sickness Benefits, Maternity Benefits.

- Significance: Supports accurate tracking of benefit-related expenses and forecasting of fund requirements.

- Fund Source

- Purpose: Identifies the source of funding for specific transactions.

- Example: Contribution Revenue, Government Subsidies, Investment Income.

- Significance: Essential for monitoring revenue streams and ensuring fund sustainability.

- Cost Center

- Purpose: Tracks expenses by operational or organizational unit.

- Example: Administration, Benefits Processing, IT Services.

- Significance: Enables cost control and efficiency analysis.

- Activity

- Purpose: Records specific financial events or activities.

- Example: Contribution Filing, Benefit Payment, Penalty Collection.

- Significance: Ensures traceability and accountability for financial actions.

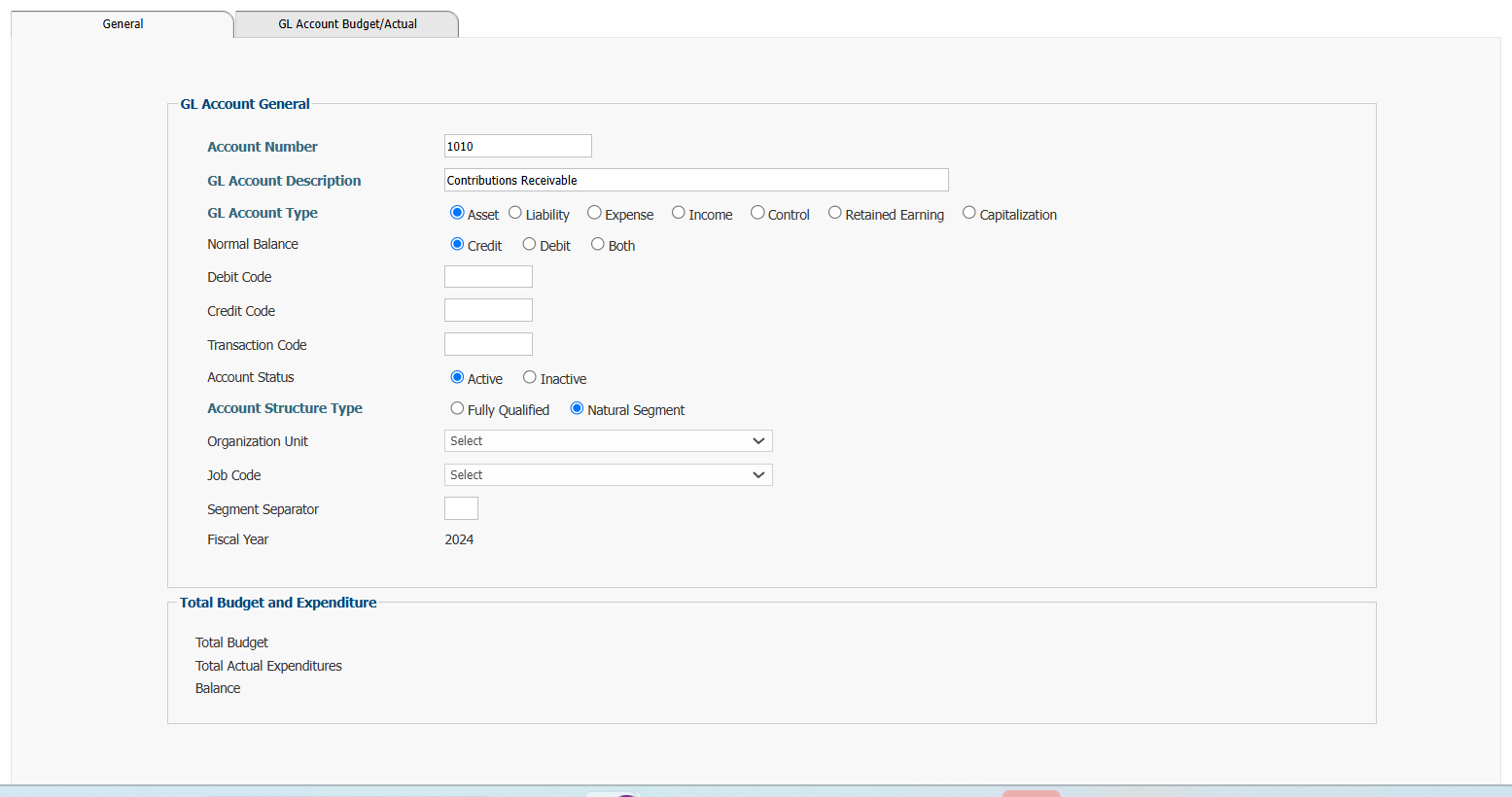

Figure 4: GL Account Defintion in Interact SSAS

Key Components of the GL Account Definition

The ability to configure granular details for GL accounts is essential for handling the complex financial activities of a social security administration, such as contributions, penalties, and benefit payments. Each attribute in the configuration provides a foundation for accurate reporting and decision-making.

- GL Account Number and Description

- Purpose:

- The Account Number uniquely identifies each GL account, ensuring no overlap or confusion in financial reporting.

- The Account Description clarifies the specific purpose of the account (e.g., “Contributions Receivable”), making it easier for administrators to interpret transactions and financial statements.

- Impact:

- Streamlines reporting by clearly categorizing income, expenses, assets, and liabilities.

- GL Account Type

- Types:

- Asset: Tracks resources like cash or receivables (e.g., Contributions Receivable).

- Liability: Records obligations, such as unpaid benefit claims.

- Expense: Captures costs, such as pensions or sickness benefits.

- Income: Represents revenue sources like contributions or penalties.

- Significance:

- Properly classifying accounts ensures accurate calculation of financial metrics, such as net income and fund solvency.

- Example:

- Defining “Contributions Receivable” as an Asset ensures it appears in the organization’s balance sheet, not in income statements.

- Normal Balance (Debit, Credit, or Both)

- Purpose:

- Specifies whether the account typically holds a debit or credit balance.

- Impact:

- Ensures accurate transaction posting by aligning with accounting principles.

- Example:

- An Asset account (e.g., Cash) should always have a debit balance, while an Income account (e.g., Contribution Revenue) should have a credit balance.

- Transaction Code

- Purpose:

- Links the GL account to specific financial activities, such as contribution filings, payments, or benefit payouts.

- Significance:

- Prevents errors by ensuring only relevant transactions are posted to each account.

- Example:

- Contributions Receivable might be linked to the transaction code for filing contributions, while Pension Expenses would be linked to benefit payments.

- Account Status

- Purpose:

- Marks the account as Active or Inactive.

- Impact:

- Prevents outdated accounts from being used in current transactions, ensuring a clean Chart of Accounts.

- Account Structure Type

- Options:

- Natural Segment: Focuses on the core classification of the account (e.g., revenue, expense).

- Fully Qualified: Includes additional segments (e.g., regions, contribution types, benefit types) to provide granular tracking.

- Impact:

- Enhances the ability to generate detailed reports by allowing accounts to be linked with operational units, job codes, or fiscal years.

Budgets at the GL Account Level

A standout feature of GL configuration is the ability to define budgets at the account level, as shown in the screenshot. This capability enables administrators to set financial targets and monitor performance for each individual GL account.

- Total Budget

- Purpose:

- Represents the allocated amount for the account in a specific fiscal year.

- Significance:

- Acts as a financial guideline, ensuring spending or revenue collection aligns with organizational goals.

- Example:

- A “Pension Expense” account might have a budget of $10 million for the year.

- Total Actual Expenditures

- Purpose:

- Tracks the actual amount spent or earned for the account to date.

- Impact:

- Provides real-time visibility into account performance, enabling proactive adjustments.

- Example:

- If $7 million has already been spent from the “Pension Expense” account, the system reflects this as the actual expenditure.

- Balance

- Purpose:

- Calculates the difference between the budget and actual expenditures.

- Significance:

- Highlights overspending or underspending, triggering alerts when limits are exceeded.

- Example:

- If only $2 million remains in the budget for pensions, administrators can plan accordingly to avoid deficits.

Alerts for Budget Control

- Automatic Notifications:

- The system can be configured to alert administrators when expenditures approach or exceed the budget.

- Impact:

- Enhances financial oversight by preventing overages and ensuring accountability.

- Example:

- If the “Sickness Benefit Expense” account is nearing its budget limit, the system generates an alert, prompting a review of benefit disbursements.

Significance for Social Security Administrations

- Improved Financial Oversight

- Detailed GL configurations and budget tracking ensure that every transaction is categorized and monitored accurately.

- Administrators can quickly identify variances and take corrective action.

- Enhanced Transparency and Accountability

- Budget tracking at the account level demonstrates fiscal discipline to stakeholders, including governments, auditors, and the public.

- Alerts and real-time reporting ensure all financial activities are documented and justifiable.

- Strategic Decision-Making

- Granular tracking of contributions and benefit payments allows for better forecasting and resource allocation.

- Enables administrators to adjust budgets dynamically based on actual expenditures and revenue trends.

Examples of Use in Social Security GL Transactions

Scenario 1: Contributions Receivable

When contributions are filed:

- The “Contributions Receivable” account (Asset) records the amount due, while the “Contribution Revenue” account (Income) reflects the anticipated income.

Example Entry:

| Account Number | Description | Debit (Dr) | Credit (Cr) |

| 1010 | Contributions Receivable | $10,000 | |

| 4010 | Contribution Revenue | $10,000 |

Scenario 2: Benefit Payments

When pensions are paid out:

- The “Pension Expense” account (Expense) is debited, and the “Cash” account (Asset) is credited.

Example Entry:

| Account Number | Description | Debit (Dr) | Credit (Cr) |

| 5010 | Pension Expense | $8,000 | |

| 1010 | Cash | $8,000 |

Scenario 3: Budget Control

The budget for the “Pension Expense” account is set at $10 million for the fiscal year:

- If actual expenditures reach $9.5 million, the system generates an alert to warn administrators of the remaining $500,000 balance.

The ability to configure GL accounts in detail, as demonstrated in the attached example, is a cornerstone of effective financial management for social security administrations. Coupled with account-level budgets and expenditure tracking, these configurations ensure transparency, accountability, and fiscal discipline. By leveraging these tools, social security systems can better manage contributions and benefit payments, maintain solvency, and uphold trust with stakeholders.

Steps in the GL Posting Process

- Configuration:

- Select the GL system in the general setup.

- Define fiscal years, periods, and Chart of Account structures.

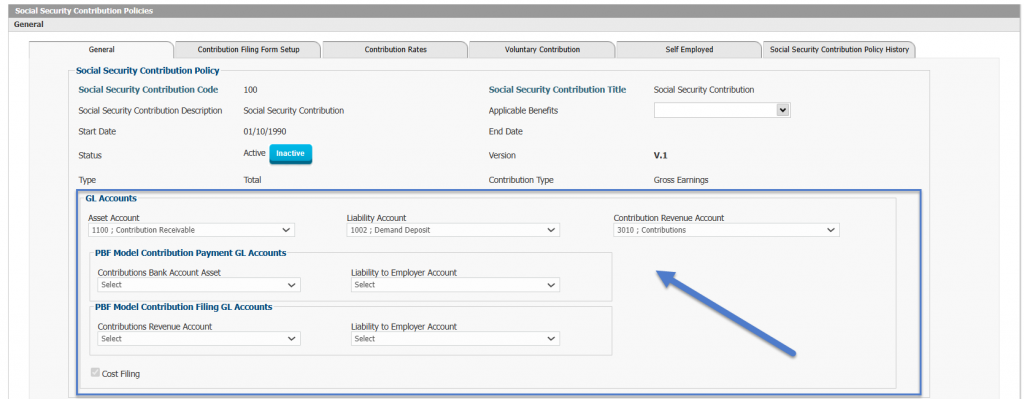

Figure 5: Linking GL Accounts with Contribution Policies

- Linking Policies:

- Associate contributions, penalties and all other receivables, as well as benefit payments and all other payables with appropriate GL accounts.

- Processing Contributions, Penalties and other Receivables:

- Generate trial journal entries for all contribution payments, penalties and other receivables received.

- Review and verify entries for accuracy before posting.

- Processing Benefit Payments and any other Payables:

- Generate trial journal entries for benefit claims and any other Payables in the current pay run.

- Exclude any payments not yet ready for processing.

- Final Posting:

- Generate the final GL file after verifying and approving trial entries and processing payments.

Integration with External GL Systems

- The GL interface uses predefined templates to generate files compatible with external systems.

- Files can be imported into commercial or legacy systems, ensuring seamless data flow.

Example: How Interact SSAS Supports Social Security Administrations

Scenario: Processing Contribution Payments

A social security agency processes monthly contributions from employers and employees. These transactions must be recorded in the GL to differentiate between:

- Cash received.

- Contributions receivable.

- Revenue from contributions.

- Penalties for late payments.

Using Interact SSAS:

- The agency configures the GL interface to match its Chart of Accounts.

- Contributions are processed, and trial GL journal entries are generated.

- After review, final entries are posted to the external GL system.

- Financial reports are generated, consolidating data for internal and external stakeholders.

Conclusion

A seamless GL interface is vital for social security administrations to maintain accurate financial records, meet complex reporting requirements, and ensure the long-term viability of investment funds. Tools like Interact SSAS offer the flexibility and automation needed to navigate diverse accounting systems, handle high transaction volumes, and deliver reliable financial data. As social security systems continue to evolve, investing in robust GL integration capabilities is not just an operational necessity—it is a cornerstone of financial sustainability and public trust.