Survivor pensions are a vital component of social security systems, designed to provide financial support to the dependents of deceased individuals. While these benefits ensure dignity and stability for survivors, they are also susceptible to fraud, creating significant costs for pension systems. This blog delves into the origins, importance, and geographic prevalence of survivor pensions, highlights fraud risks, and explores the unique capabilities of Interact SSAS in managing survivor pensions, including calculations, compliance, and case management.

Fraud Risks in Survivor Pensions and Their Costs

Survivor pensions are a lifeline for beneficiaries, but they can also attract fraudulent activity. Common types of fraud include:

- False Relationship Claims: Individuals may falsely claim to be spouses, children, or dependents of the deceased.

- Non-Reported Remarriages: Spouses who remarry but fail to report their new status to continue receiving benefits.

- Deceased Not Reported: Families may conceal the death of a survivor to continue receiving their survivor benefits.

- Forged Documentation: Fake death certificates, marriage certificates, or birth certificates may be submitted to support fraudulent claims.

The cost of such fraud is immense. It not only depletes resources meant for genuine beneficiaries but also erodes public trust in social security systems. Inaccurate disbursements can lead to budgetary shortfalls, forcing systems to reassess their policies or increase contributions. Effective tools like Interact SSAS help mitigate these risks through robust compliance and case management capabilities.

The Evolution and Importance of Survivor Pensions

Originating in the early 20th century, survivor pensions were first introduced as part of broader welfare reforms in Europe to protect families from destitution. Today, these pensions represent a commitment to socio-economic equity, ensuring survivors can maintain a basic quality of life. They also serve a broader societal function, reducing poverty and dependence on alternative public assistance.

Global Prevalence of Survivor Pensions

The structure and reach of survivor pensions vary widely across regions, influenced by economic development, cultural norms, and the extent of social security infrastructure. Below is a detailed exploration of how survivor pensions operate across various geographies:

Europe

Europe leads in providing comprehensive survivor pension systems, often fully integrated into national social security frameworks. Key features include:

- Universal Coverage: Most European countries ensure that all citizens are eligible, regardless of employment history. Systems like Germany’s gesetzliche Rentenversicherung (statutory pension insurance) and the UK’s State Pension include survivor benefits for spouses, children, and dependents.

- Customizable Entitlements: Benefits are tailored based on the survivor’s relationship with the deceased. For instance, in France, widows and widowers may receive a portion of the deceased’s pension if they meet certain age and dependency criteria.

- Generous Provisions for Children: Many countries offer benefits until children reach adulthood or complete higher education, with additional support for orphans and disabled dependents.

North America

Survivor benefits in North America are primarily tied to the deceased’s work history and contributions to national pension schemes:

- United States: Survivor benefits under Social Security depend on the deceased’s earnings record. Eligible survivors include spouses, children, and in some cases, parents. Spousal benefits typically start at age 60 (or 50 for disabled spouses), and children are eligible until age 18 (or 19 if still in school).

- Canada: The Canada Pension Plan (CPP) provides survivor pensions, lump-sum death benefits, and benefits for dependent children. Eligibility is closely linked to the deceased’s CPP contributions, and the benefits are subject to age and relationship status.

Asia

Asia presents a diverse picture, with significant differences between developed and developing countries:

- Developed Nations: Japan and South Korea have robust survivor pension systems. Japan’s Kosei Nenkin (employees’ pension insurance) provides survivor pensions to spouses, children, and dependent parents of deceased contributors. South Korea’s National Pension Scheme offers similar benefits, with provisions for remarried spouses and continued education for dependent children.

- Emerging Economies: India’s Employee Provident Fund Organization (EPFO) includes a survivor pension for families of formal sector workers. However, coverage is limited, with many informal sector workers excluded. Similarly, in countries like the Philippines, benefits under the Social Security System (SSS) are restricted to contributors, leaving gaps for non-covered populations.

Africa

In Africa, survivor pensions are often part of broader social insurance schemes, but coverage remains uneven:

- Sub-Saharan Africa: Countries like South Africa and Kenya have survivor benefits tied to formal employment. South Africa’s Unemployment Insurance Fund (UIF) includes death benefits for dependents of contributors, while Kenya’s National Social Security Fund (NSSF) provides lump-sum payouts rather than ongoing pensions.

- Challenges: Informal employment dominates in many African nations, limiting access to survivor pensions. Some countries are experimenting with community-based insurance schemes to bridge the gap, but these remain underfunded and inconsistent.

Latin America

Survivor pensions in Latin America are evolving, reflecting shifts toward universal principles in some nations:

- Established Systems: Chile’s privatized pension model includes survivor benefits funded through individual accounts, with provisions for spouses, children, and dependent parents. Brazil offers survivor pensions through its Instituto Nacional do Seguro Social (INSS), with benefits based on the deceased’s contribution record.

- Emerging Reforms: Countries like Mexico are expanding their systems to cover informal workers. Survivor pensions under the Instituto Mexicano del Seguro Social (IMSS) now extend to non-contributory beneficiaries in certain cases, signaling a move toward inclusivity.

The Caribbean

Survivor pensions in the Caribbean are often managed by national insurance boards, reflecting a blend of universal and employment-based principles:

- Comprehensive Coverage: Nations like Barbados and Trinidad and Tobago offer survivor benefits through their national insurance schemes. These systems provide pensions or lump-sum payments to spouses, children, and dependent parents.

- Tourism and Informal Employment: High levels of informal employment in many Caribbean nations create challenges for broad coverage. Some countries, like Jamaica, are working to integrate informal workers into their national insurance frameworks to expand survivor benefits.

- Flexible Definitions of Dependents: The Caribbean systems often recognize extended family structures, allowing dependent grandparents or siblings to qualify for benefits in the absence of closer relatives.

Interact SSAS: A Comprehensive Platform for Survivor Pensions

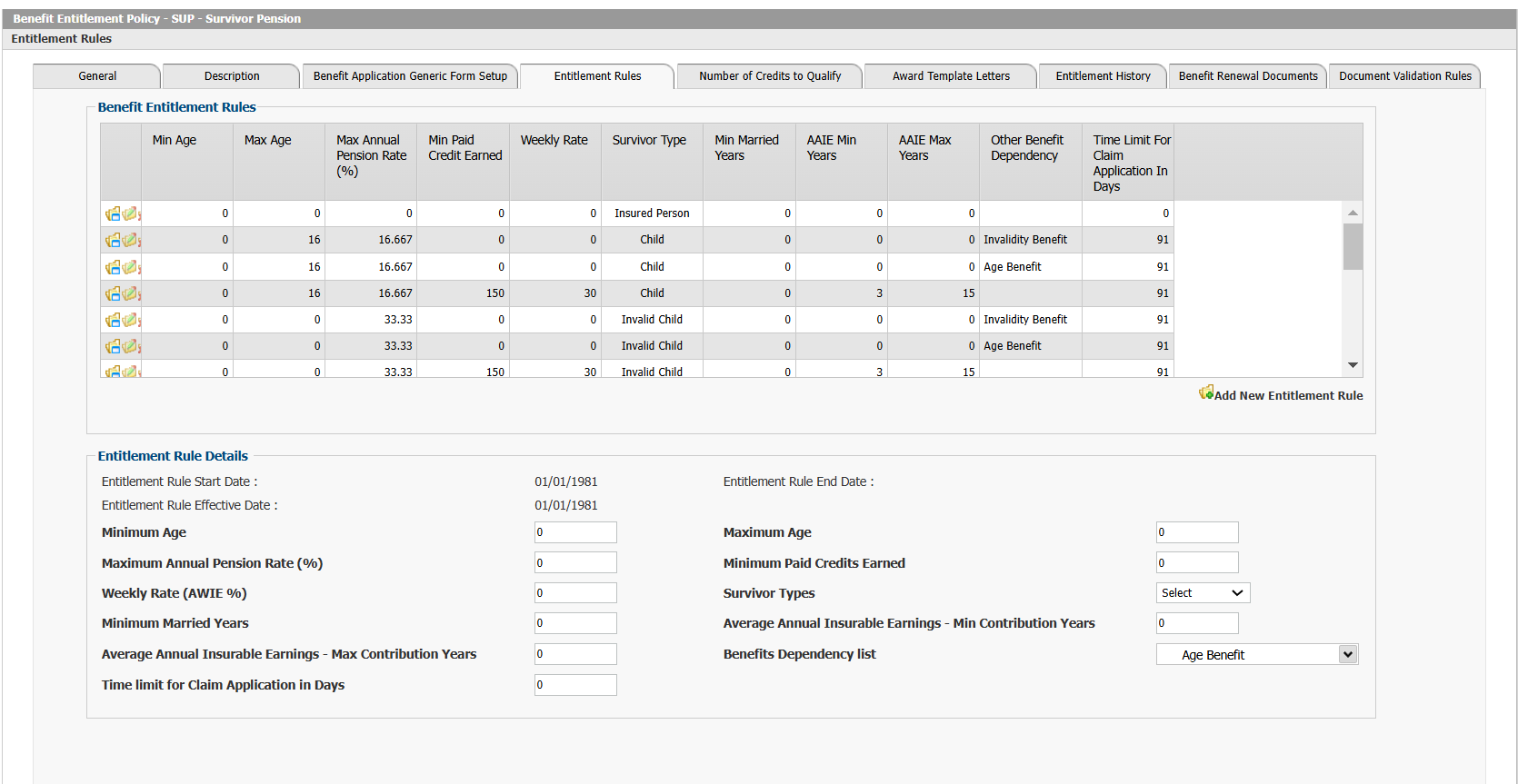

Figure 1: Survivor Benefit Entitlement Rate Table Configuration

Interact SSAS provides a sophisticated platform for managing survivor pensions, offering unparalleled flexibility, compliance features, and case management tools.

Key Features and Configuration

- Policy and Benefit Class Configuration:

- Administrators define benefit classes to include all parameters, such as eligibility rules, entitlement rates, and renewal conditions. Policies specify the beneficiaries’ categories and rates.

- Eligibility and Documentation:

- Eligibility is determined based on the Rate Table parameters originally included under the Benefit Class definition. This eligibility includes relationships like spouse, children (with special rules for orphans and invalid children), parents, grandparents and other dependents. Document requirements, such as death and birth certificates, are enforced with validation rules.

- Dynamic Rate Management:

- The platform supports variable rates for survivors:

- A spouse may receive 50% of the deceased’s pension.

- Children may share an additional 50%, divided equally.

- Rates for children with disabilities can differ, reflecting higher dependency needs.

- The platform supports variable rates for survivors:

- Renewal and Compliance Enforcement:

- Survivors must provide updated documents, such as school enrollment certificates for children above a certain age, annual life certificates for survivors themselves, or medical reports, to continue receiving benefits.

- Adjustment Management

- Once a survivor pension entitlement is approved, any changes or corrections needed can be processed as an adjustment.

- Adjustment Scenarios:

- Increase or decrease in benefits due to regulatory changes, additional eligible survivors, or rectification of errors.

- Backdated adjustments to account for missed entitlements.

- Change in status of beneficiaries, such as a child becoming ineligible upon leaving school or a spouse remarrying.

- Adjustments ensure survivors receive accurate benefits while maintaining compliance with policies and regulations.

- Third-Party Payables Integration

- Debt Management: The system allows integration with other government entities or creditors to manage situations where beneficiaries owe money.

- For example, if a court order mandates garnishment, a portion of the benefit can be redirected to pay a third-party creditor (e.g., child support, tax arrears).

- Automation:

- The system ensures accurate and timely deductions from survivor benefits.

- Transparent tracking of payments ensures beneficiaries and payees have clear records.

- Minimum Pension Rules

- Minimum Pension Application:

- Survivor benefits can incorporate minimum pension rules, ensuring a base level of financial support.

- Exemptions:

- Certain exemptions may apply, such as in cases of the “No Two Full Pension Rule.”

- If the deceased’s underlying pension was already subject to minimum pension rules, additional adjustments may be disallowed.

- This prevents duplicate or unwarranted applications of minimum thresholds, maintaining equity and compliance.

- Suspension of Pensions

- Suspension Scenarios:

- Pensions can be suspended if anomalies are detected, such as:

- Invalid documents (e.g., fake death certificates).

- Fraudulent claims.

- Non-compliance with rules, such as failure to submit a required school enrollment certificate for a child.

- Pensions can also be suspended temporarily during investigations or due to court orders.

- Pensions can be suspended if anomalies are detected, such as:

- Benefits of Suspension:

- Protects funds and ensures benefits are disbursed only to eligible survivors.

- Error Recovery Through Receivables

- Incorrect or Overpaid Benefits:

- If benefits are paid in error (e.g., to an ineligible survivor or due to calculation mistakes), the system can initiate recovery.

- Receivables Module:

- An invoice is raised to the beneficiary for the incorrect or overpaid amount.

- The module tracks repayments and integrates with benefit management, ensuring accurate financial reconciliation.

- Flexible Recovery Options:

- Recovery can be adjusted to allow partial repayments or deductions from future benefits.

Example of Survivor Pension Calculation

Using Interact SSAS consider the following scenario:

- Deceased Pensioner: Eligible for $2,000 monthly.

- Survivors:

- Spouse: Entitled to 50%.

- Two children: Share the remaining 50% equally.

Calculation:

- Spouse’s Benefit: 50%×$2,000=$1,000

- Each Child’s Benefit: 25%×$2,000=$500 each

Total monthly disbursement to the survivors would be:

- Spouse: $1,000

- Child 1: $500

- Child 2: $500

This example illustrates how the system handles dynamic rate allocation based on policy definitions.

Case Management in Interact SSAS

Fraudulent claims and discrepancies require thorough investigation to maintain system integrity. Interact SSAS incorporates advanced case management tools to handle these scenarios effectively:

- Flagging Inconsistencies:

- Claims with missing or suspicious documentation are flagged for review. For instance, a death certificate that does not match national registry records triggers an investigation. The person reviewing the claim can open a case associated with the claim and the case will be assigned to a case officer who can investigate further or close the case.

- Investigation Workflow:

- Case managers can:

- Assign investigations to specialized staff.

- Collect additional documents from claimants.

- Access historical data and audit trails to identify patterns of fraud.

- Case managers can:

- Adjudication and Resolution:

- After the investigation, the claim is adjudicated. If discrepancies are resolved, the claim proceeds. Otherwise, it may be denied, or legal action initiated.

- Collaboration and Transparency:

- The system facilitates collaboration among stakeholders, ensuring transparency in decision-making.

Ensuring Compliance with Interact SSAS

Compliance is a cornerstone of survivor pension systems, preventing fraud and ensuring equitable benefit distribution. Interact SSAS excels in this area with:

- Regulatory Adherence:

- The platform accommodates diverse legal frameworks, including recognition of different marriage types (e.g., common law, extended cohabitation).

- Audit Trails:

- Detailed logs provide a clear record of all system interactions, supporting audits and regulatory reviews.

- Periodic Document Validation:

- Rules enforce the submission of renewal documents, such as school enrollment or dependency certificates, ensuring ongoing eligibility.

- Automated API Integration:

- The SSAXML API connects with national registries, automating data verification to prevent fraudulent claims.

Unique Features of Interact SSAS

Interact SSAS offers capabilities that set it apart:

- Guardian Claims:

- For minors, benefits can be claimed by guardians, with oversight to ensure funds are used appropriately.

- Survivor Portals:

- Beneficiaries can submit claims, track progress, and upload documents via an intuitive portal.

- Scalability:

- The platform supports organizations of any size, with configurations tailored to specific regional or organizational needs.

- Customizable Reporting:

- Detailed analytics and reporting tools provide insights into benefit distribution trends, compliance rates, and fraud detection efficiency.

Conclusion

Survivor pensions are indispensable for supporting vulnerable populations, but they require robust systems to manage complexity and prevent fraud. Interact SSAS combines flexibility, compliance, and case management to meet these challenges. By leveraging features like dynamic rate allocation, thorough documentation validation, and case investigation tools, organizations can ensure that benefits are distributed fairly and efficiently.

The commitment to compliance and adaptability makes Interact SSAS a standout solution for administering survivor pensions, safeguarding resources, and maintaining public trust in social security systems.