Using Interact SSAS to Empower and Support Self-Employed Workers: A Comparative Analysis of Social Security Rules in the Caribbean, US, Canada, and the UK

Self-employment is a vital pillar of many economies, offering individuals the opportunity to work independently while contributing to national development. However, self-employed workers often face unique challenges when it comes to social security systems, as they must navigate contribution rules without the benefit of employer assistance. In this blog, we delve into the social security rules for self-employed individuals in the Caribbean and contrast them with systems in the United States, Canada, and the United Kingdom.

The Caribbean: Supporting Self-Employed Workers in Small Economies

Social security systems in the Caribbean are designed to address the unique needs of small, often island-based economies. These systems focus on ensuring coverage for all contributors, including self-employed individuals, while balancing the challenges of limited resources.

Key Features of Social Security for Self-Employed in the Caribbean:

- Mandatory Registration:

- Self-employed individuals must register with their respective national social security boards.

- Registration typically requires personal information, proof of self-employment, and estimated earnings.

- Contribution Rates:

- Contribution rates vary across countries but are generally based on a percentage of declared or insurable earnings.

- For example:

- Dominica: Self-employed individuals contribute 13.25% of their declared earnings as of 2024.

- Antigua and Barbuda: The rate is 10% of declared earnings.

- Barbados: Self-employed contributions are categorized into National Insurance (13.5%), Non-Contributory (2%), Training Levy (0.5%), Catastrophe Fund (0.1%), and Health Service Contribution (1%), totaling 17.1%.

- Income Declaration:

- Self-employed workers are required to declare their income periodically (monthly, quarterly, or annually), with minimum and maximum thresholds guiding contribution amounts.

- Benefits:

- Contributions entitle self-employed workers to pensions, sickness benefits, maternity benefits, and more, depending on the country.

- For example, in Barbados, contributions also provide unemployment insurance.

- Reassessment and Adjustments:

- Workers can reassess their declared income annually, typically within a designated window (e.g., January).

- In some countries, adjustments must align with set percentages or increments.

- Voluntary Contributions:

- Some Caribbean nations, such as Saint Kitts and Nevis, allow previously employed individuals to switch to voluntary contributions to maintain benefits eligibility.

Strengths and Challenges in the Caribbean Model:

- Strengths:

- Inclusive systems ensure all workers, including the self-employed, have access to essential social benefits.

- Flexibility in income declaration accommodates diverse economic realities.

- Challenges:

- Compliance can be difficult due to informal economies.

- Limited resources may restrict benefit payouts or expansion.

The United States: Balancing Autonomy with Responsibility

The United States follows a dual-purpose approach for self-employed individuals, incorporating both Social Security and Medicare through the Self-Employment Contributions Act (SECA).

Key Features of the US Model:

- Self-Employment Tax (SE Tax):

- Self-employed individuals are responsible for paying both the employer and employee portions of Social Security (12.4%) and Medicare (2.9%), totaling 15.3%.

- Income Limits:

- Social Security contributions apply to annual earnings up to $176,100 (2025). There is no cap for Medicare contributions.

- Reporting and Payment:

- Self-employed individuals report earnings and calculate SE tax on Schedule SE (Form 1040). Payments are made alongside annual tax filings or via quarterly estimated taxes.

- Deductions:

- Half of the SE tax is deductible, reducing taxable income and offering some financial relief.

- Benefits:

- Contributions count toward Social Security benefits, including retirement, disability, and survivors’ benefits. Medicare coverage is also ensured.

Strengths and Challenges in the US Model:

- Strengths:

- Simplified, standardized processes for calculating and reporting SE tax.

- Comprehensive benefits tied directly to contribution history.

- Challenges:

- High tax burden due to dual responsibilities.

- Limited options for voluntary contributions, leaving gaps for intermittent workers.

Canada: A Dual Contribution for Self-Employed Individuals

Canada’s approach to self-employment focuses on contributions to the Canada Pension Plan (CPP), with additional provisions for Employment Insurance (EI) on an optional basis.

Key Features of the Canadian Model:

- CPP Contributions:

- Self-employed individuals pay both the employee and employer portions, totaling 11.9% of net self-employment income (2025).

- Contributions are calculated on earnings above a $3,500 exemption and below a maximum pensionable earnings cap ($81,200 for 2025).

- Optional EI Contributions:

- Self-employed workers may opt into EI, offering access to benefits such as parental leave and sickness benefits.

- Reporting and Payment:

- Contributions are reported on Schedule 8 of the T1 tax return and paid annually.

- Benefits:

- CPP contributions entitle self-employed individuals to retirement pensions, disability benefits, and survivor benefits.

- EI opt-ins provide additional coverage for specific life events.

Strengths and Challenges in the Canadian Model:

- Strengths:

- Optional EI contributions add flexibility for workers with varying needs.

- CPP contributions ensure a secure retirement foundation.

- Challenges:

- High combined contribution rates can strain limited incomes.

- Opt-in processes for EI require careful planning to balance cost and coverage.

The United Kingdom: Simplicity with a Tiered System

The UK National Insurance (NI) system provides a simplified yet tiered approach for self-employed contributions, focusing on affordability and essential benefits.

Key Features of the UK Model:

- Class 2 and Class 4 Contributions:

- Self-employed individuals pay:

- Class 2 NI: Flat weekly rate (£3.45 for 2025) for earnings above £12,570.

- Class 4 NI: Percentage of annual profits (9% on profits between £12,570 and £50,270; 2% above this threshold).

- Self-employed individuals pay:

- Reporting and Payment:

- Contributions are calculated as part of the annual Self Assessment tax return and paid to HM Revenue & Customs (HMRC).

- Benefits:

- Contributions qualify individuals for the State Pension and other benefits, such as maternity allowance.

Strengths and Challenges in the UK Model:

- Strengths:

- Clear differentiation between mandatory and income-dependent contributions.

- Lower flat-rate contributions make the system accessible for low earners.

- Challenges:

- Limited benefits compared to more robust systems like Canada’s CPP.

- Complex thresholds can confuse first-time contributors.

Comparative Analysis: Caribbean vs. US, Canada, and UK Models

| Feature | Caribbean | US | Canada | UK |

| Registration | Mandatory | Mandatory | Mandatory | Mandatory |

| Contribution Rates | Varies (10–13.25%) | 15.3% (SECA) | 11.9% (CPP); optional EI | Class 2 (£3.45/week); Class 4 (9–2%) |

| Income Declaration | Periodic | Annually (Form 1040, Schedule SE) | Annually (Schedule 8, T1) | Annually (Self Assessment) |

| Benefits | Pensions, sickness, maternity | Social Security, Medicare | CPP benefits; optional EI benefits | State Pension, maternity allowance |

| Voluntary Contributions | Allowed (some countries) | Not allowed | Not allowed | Not applicable |

| Strengths | Inclusive, tailored to small economies | Comprehensive benefits | Optional EI provides flexibility | Accessible for low-income earners |

| Challenges | Informal economies hinder compliance | High tax burden | High combined rates for CPP/EI | Limited benefits for high contributors |

Empowering and Supporting Self-Employed Individuals through Interact SSAS

Interact SSAS provides comprehensive support for self-employed individuals to manage their contributions efficiently. Here’s a detailed breakdown of its functionality, covering registration, declaring earnings, assessment and re-assessment, payment of contributions, and claiming benefits:

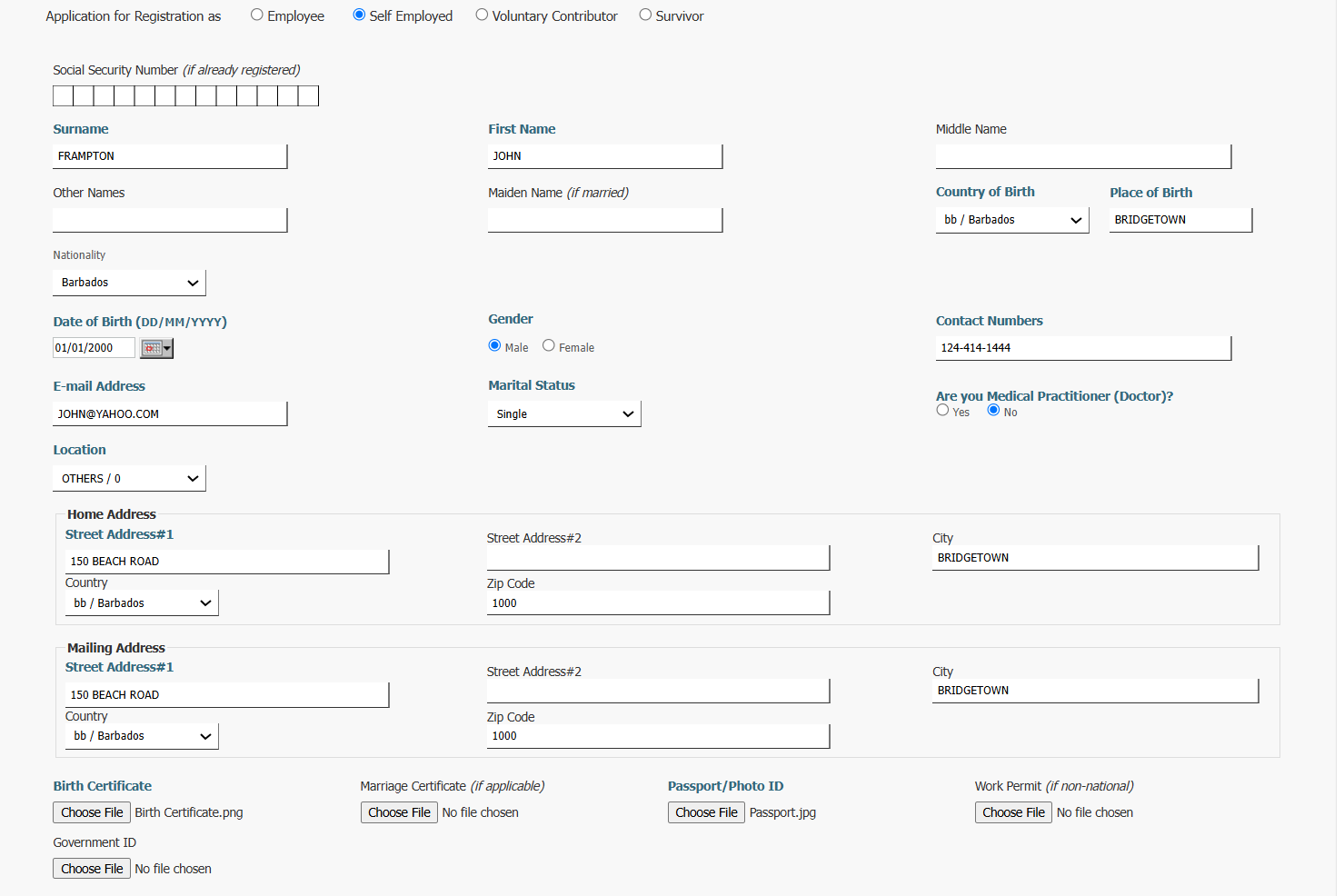

Registration for Self-Employed Individuals

- Application Process: Self-employed individuals use the system to register for social security contributions. Registration requires personal and business details, such as name, occupation, business address, and commencement date.

- Document Upload: Necessary documents like birth certificates, marriage certificates, and photo IDs can be uploaded directly through the system.

- Automated Validation: The system validates entries and documents, ensuring compliance with local regulations before approval.

Declaring Earnings

- Annual and Monthly Declarations: Self-employed individuals declare their annual or monthly earnings, which form the basis for calculating insurable earnings.

- Validation Against Limits: If declared earnings fall below the minimum or exceed the maximum set limits, the system issues alerts. Users can adjust or confirm entries as required.

- Editable Fields: Earnings and job-related details can be updated based on changing circumstances, ensuring accurate contributions.

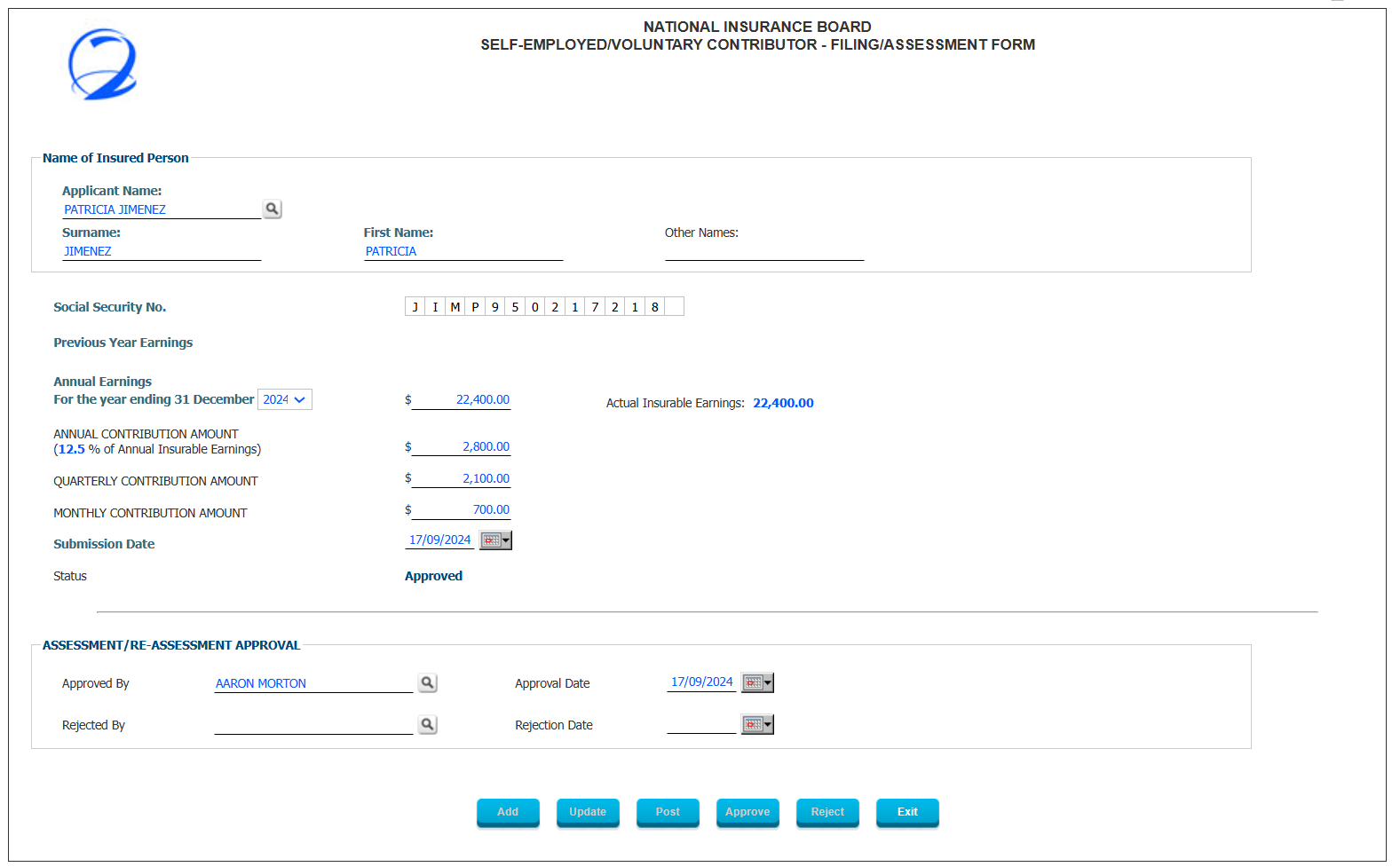

Assessment and Re-Assessment

- Initial Assessment: Contribution amounts are automatically calculated as a percentage of declared earnings. The system provides annual, quarterly, and monthly breakdowns.

- Re-Assessment Triggers: Re-assessments occur when there are significant changes in declared earnings or discrepancies in initial assessments.

- Approval Workflow: Assessments and re-assessments must be approved by designated personnel. The system tracks approval or rejection statuses.

- Automated Alerts: If re-assessments exceed the allowable number for a year or involve significant changes, the system provides warnings to ensure compliance.

Payment of Contributions

- Integrated Payment Options: Contributions can be paid online through the system. Multiple payment methods, including cash, bank transfers, and credit cards, are supported.

- Pending Payment Alerts: The dashboard highlights pending contributions in bold, allowing users to prioritize them.

- Real-Time Status Updates: Payment statuses are updated automatically, reflecting whether contributions are “Initiated,” “Processed,” or “Completed.”

- Flexible Period Selection: Payments can be made for selected periods, accommodating individual preferences and cash flow situations.

Claiming and Receiving Benefits

- Eligibility Validation: The system cross-references contribution histories to determine eligibility for benefits like pensions, sickness allowances, and maternity benefits.

- Simplified Claims Process: Claim forms auto-populate with existing data, reducing manual entry errors.

- Approval and Disbursement: Benefits claims go through an approval process before disbursements are processed through linked bank accounts or other payment methods.

Additional Features

- Automated Processes: Annual contribution filings are generated automatically if the user fails to submit on time, ensuring continuity.

- Self-Service Dashboard: Users can track their contributions, payment history, and benefit claims through an intuitive interface.

- Support for Voluntary Contributions: Those transitioning from employment to voluntary contributions can easily register and continue their coverage.

- Reports and Analytics: The system generates detailed reports on contributions, payments, and benefits for better financial planning.

Conclusion

The social security systems in the Caribbean, US, Canada, and the UK reflect diverse approaches tailored to their respective economic and social contexts. Caribbean systems prioritize inclusivity and adaptability, while the US focuses on comprehensive coverage despite a higher tax burden. Canada offers flexibility with optional EI contributions, and the UK ensures simplicity with flat-rate contributions.

For self-employed individuals, understanding these systems is essential for effective planning and compliance. Whether you are navigating a small Caribbean economy or the larger frameworks of the US, Canada, or the UK, being informed about contribution rules and benefits is key to ensuring financial security in the years ahead.

Interact SSAS simplifies the complex processes associated with self-employed social security management, ensuring compliance, transparency, and accessibility for users. This holistic approach supports both the contributors and the administration, fostering a seamless social security experience.